Featured

Table of Contents

- – What types of Lifetime Income Annuities are av...

- – What should I know before buying an Guaranteed...

- – Are Retirement Income From Annuities a safe i...

- – Who provides the most reliable Tax-efficient ...

- – What does an Guaranteed Income Annuities inc...

- – How does an Annuity Contracts help with reti...

For those ready to take a little bit more threat, variable annuities supply additional chances to expand your retired life possessions and possibly boost your retirement earnings. Variable annuities supply a variety of investment choices supervised by professional money managers. Therefore, capitalists have a lot more versatility, and can even move properties from one alternative to another without paying tax obligations on any kind of investment gains.

* An immediate annuity will not have a buildup stage. Variable annuities released by Protective Life insurance policy Firm (PLICO) Nashville, TN, in all states except New york city and in New York by Protective Life & Annuity Insurance Provider (PLAIC), Birmingham, AL. Stocks used by Investment Distributors, Inc. (IDI). IDI is the major underwriter for registered insurance policy products issued by PLICO and PLAICO, its affiliates.

Capitalists need to thoroughly consider the financial investment objectives, dangers, charges and costs of a variable annuity and the underlying financial investment choices before investing. This and other details is contained in the prospectuses for a variable annuity and its underlying investment alternatives. Syllabus might be obtained by contacting PLICO at 800.265.1545. An indexed annuity is not an investment in an index, is not a protection or supply market investment and does not join any supply or equity financial investments.

What's the difference between life insurance policy and annuities? It's a typical concern. If you question what it takes to secure an economic future for yourself and those you like, it might be one you locate yourself asking. Which's a very good thing. The lower line: life insurance policy can aid offer your liked ones with the financial comfort they are worthy of if you were to die.

What types of Lifetime Income Annuities are available?

Both need to be considered as part of a long-term monetary plan. Although both share some similarities, the general function of each is very different. Allow's take a fast look. When comparing life insurance policy and annuities, the largest difference is that life insurance policy is developed to assist shield against an economic loss for others after your death.

If you wish to discover much more life insurance policy, reviewed up on the specifics of how life insurance policy functions. Consider an annuity as a tool that could aid fulfill your retired life requirements. The primary function of annuities is to create income for you, and this can be done in a couple of different methods.

What should I know before buying an Guaranteed Income Annuities?

There are numerous potential benefits of annuities. Some include: The ability to grow account worth on a tax-deferred basis The possibility for a future income stream that can not be outlasted The possibility of a lump sum advantage that can be paid to a making it through spouse You can get an annuity by giving your insurance provider either a solitary swelling sum or making payments in time.

People usually get annuities to have a retirement earnings or to construct financial savings for an additional function. You can purchase an annuity from an accredited life insurance policy representative, insurance business, economic organizer, or broker. You must speak with a financial advisor concerning your requirements and objectives prior to you get an annuity.

Are Retirement Income From Annuities a safe investment?

The difference between the two is when annuity payments begin. You do not have to pay taxes on your profits, or payments if your annuity is a specific retirement account (IRA), until you withdraw the incomes.

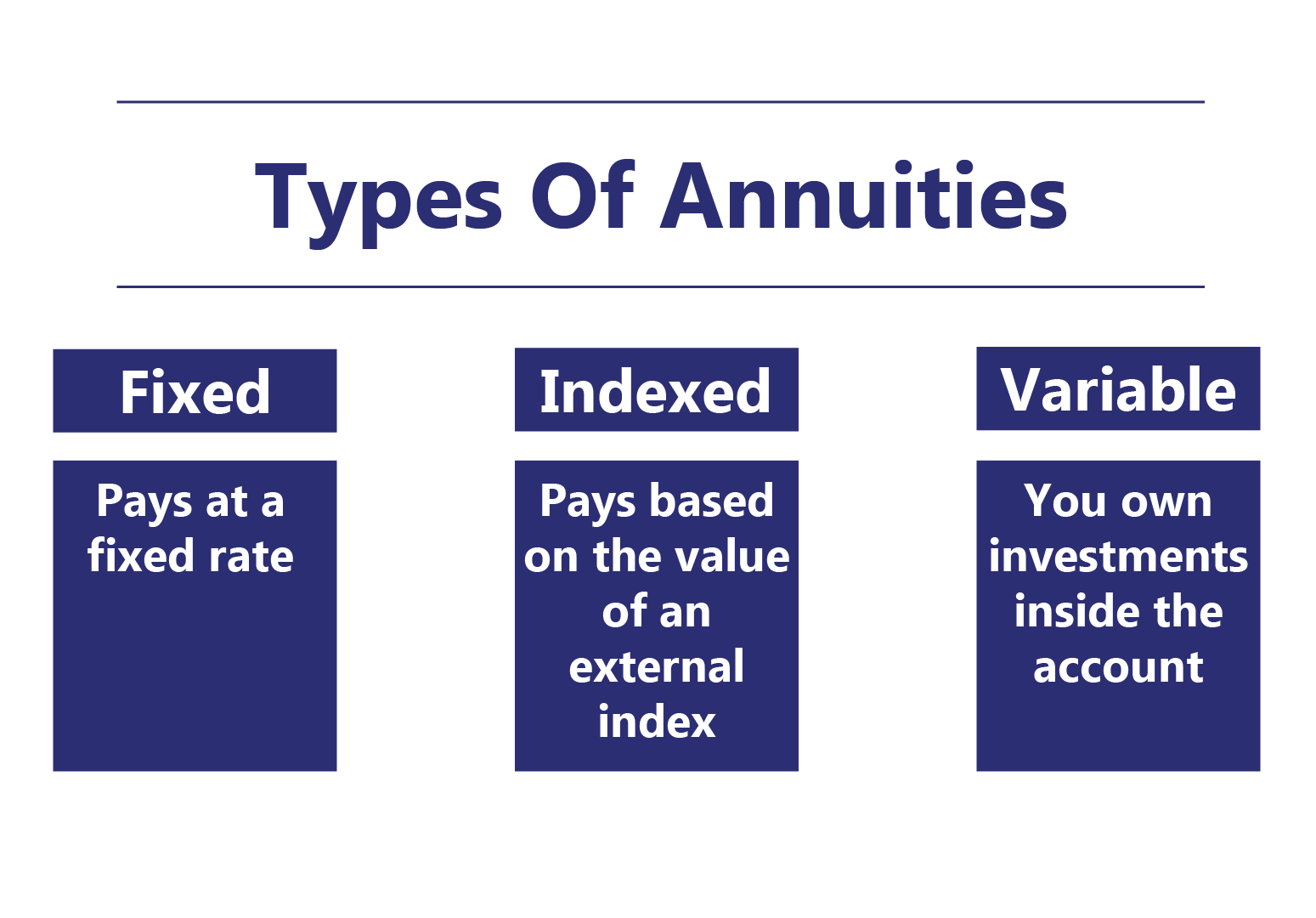

Deferred and instant annuities offer several choices you can select from. The alternatives offer various levels of potential danger and return: are assured to make a minimum rate of interest. They are the least expensive monetary danger yet offer lower returns. make a greater rate of interest, however there isn't an ensured minimum rate of interest.

allow you to choose between sub accounts that resemble mutual funds. You can earn much more, but there isn't an ensured return. Variable annuities are higher risk since there's an opportunity you might shed some or all of your cash. Set annuities aren't as risky as variable annuities since the financial investment danger is with the insurance provider, not you.

Set annuities guarantee a minimum interest rate, normally between 1% and 3%. The business could pay a higher passion rate than the assured interest rate.

Who provides the most reliable Tax-efficient Annuities options?

Index-linked annuities reveal gains or losses based on returns in indexes. Index-linked annuities are a lot more complicated than taken care of deferred annuities (Annuity riders).

Each depends on the index term, which is when the firm calculates the rate of interest and credit histories it to your annuity. The establishes exactly how much of the rise in the index will certainly be made use of to determine the index-linked passion. Other crucial functions of indexed annuities include: Some annuities top the index-linked rate of interest.

The flooring is the minimal index-linked rates of interest you will gain. Not all annuities have a floor. All dealt with annuities have a minimum guaranteed value. Fixed-term annuities. Some firms make use of the average of an index's worth as opposed to the worth of the index on a specified date. The index averaging may happen whenever throughout the term of the annuity.

What does an Guaranteed Income Annuities include?

The index-linked interest is included in your initial premium amount but does not substance throughout the term. Other annuities pay substance rate of interest during a term. Compound interest is rate of interest earned on the money you conserved and the passion you earn. This means that rate of interest currently attributed also earns passion. In either case, the interest gained in one term is generally intensified in the next.

If you take out all your cash prior to the end of the term, some annuities won't credit the index-linked passion. Some annuities could attribute only part of the passion.

How does an Annuity Contracts help with retirement planning?

This is due to the fact that you birth the investment risk as opposed to the insurance provider. Your agent or financial consultant can aid you determine whether a variable annuity is appropriate for you. The Securities and Exchange Commission identifies variable annuities as protections because the efficiency is originated from stocks, bonds, and other financial investments.

An annuity contract has 2 stages: a buildup phase and a payout phase. You have numerous options on how you contribute to an annuity, depending on the annuity you get: allow you to select the time and quantity of the settlement.

{kind=link}

Table of Contents

- – What types of Lifetime Income Annuities are av...

- – What should I know before buying an Guaranteed...

- – Are Retirement Income From Annuities a safe i...

- – Who provides the most reliable Tax-efficient ...

- – What does an Guaranteed Income Annuities inc...

- – How does an Annuity Contracts help with reti...

Latest Posts

How can an Lifetime Payout Annuities protect my retirement?

How do I receive payments from an Fixed Indexed Annuities?

How much does an Secure Annuities pay annually?

More

Latest Posts

How can an Lifetime Payout Annuities protect my retirement?

How do I receive payments from an Fixed Indexed Annuities?

How much does an Secure Annuities pay annually?